Commentary

Kaleel Communique is an email series delivering ideas, information and strategies specifically for uncommonly successful people.

Summer Thoughts on a Foggy Economy (July 28, 2020)

The Stock Market, the Economy, and the Virus (April 13,2020)

Update on Market Sell-off (March 10,2020)

The Coronavirus and the Election of 2020 (March 3, 2020)

The Yield Curve, a Recession, and Thoughts about the Future (Oct 2019)

Market Thoughts and Update (Mar 2018)

Summer Thoughts on a Foggy Economy

July 28, 2020

So much has happened since the beginning of 2020. A virus threw the US into a recession with economic growth going from +2.1% in the final quarter of 2019 to -5.1% at the end of the first quarter 2020 (Bureau of Economic Analysis, https://www.bea.gov/news/glance.) Some people might say that this was coming and are not surprised by what has transpired. Sadly, no matter how often the pandemic was predicted, this was not expected. A true Black Swan event.

This pandemic will become a marker for the 21st century and is likely to impact our daily lives for some time to come. Cottage industries of mask making have erupted, and there is no end to mask creativity. On a more serious note, how will the virus impact the economy and the stock market? Will new technologies and industries spring up? While we don’t have a crystal ball, the way we live and work has changed, and some of it will likely become permanent or accepted as normal. I’ve gotten so used to wearing a mask it feels like another piece of clothing.

Stocks don’t seem to care about the virus

Despite the current economic conditions, investors have continued to be buyers in the stock market, ignoring the surging virus in various states. Why is the stock market not reacting to the possibility of shutdowns in major states? The primary reason is that the stock market is a leading indicator and tends to focus on longer-term outcomes, possibly next year or beyond.

Also, the extremely low interest rates (the 10-year US Treasury yields approximately 0.6%) make bonds less attractive. However, bonds are still being purchased by US and foreign investors for stability. Based on what we are hearing, we expect that low interests will be here for a while. With these low rates, investors are incentivized to invest in stocks.

Choppy, choppy for awhile

We believe that the near-term stock market movements will be choppy as second quarter earnings continue to be released over the coming weeks. Forecasts for corporate earnings continue to be negative for the remainder of the year and recovering in 2021. The second quarter may show more bankruptcies, and in fact, the five largest banks in the US announced last week their plans to set aside $35 billion to prepare for what could be a wave of future defaults – mortgages, credit cards, personal loans, auto loans and corporate bankruptcies (source: CNN https://www.cnn.com/2020/04/17/business/bank-earnings-defaults-recession/index.html). This is a clear indication that the banks are in protection mode and are preparing for a worse case. If this comes to pass, the banks are ready, and if it’s not as bad as they predict, the banks will be likely to show improved earnings and strength.

Getting back into the workforce and businesses to get another bump

The re-hiring of the unemployed and furloughed, along with the ability of businesses to re-open, will be critical to the shape of the economic recovery. It took 10 years for the employment level to grow from a low of 129.7 million in February 2010 to the high of 152.5 million in February 2020. Then in only two months, we lost over 22 million jobs. The bright side is that in the last two months, employment has improved. Rehiring was evident in the data. The number of employed people grew from April’s low of 130.3 million to 133.0 million in May and in June to 134.8 million (source: https://fred.stlouisfed.org/series/PAYEMS).

The new stimulus package should be coming soon as Republicans are close to releasing their proposal. Then both parties will have to come to an agreement. Reports indicate that there will be another check of $1,200 to individuals, although the income level may be different from the first stimulus check. The coming stimulus is likely to extend unemployment benefit enhancement as the $600 per week benefit will expire on July 25th in most states. The clock is ticking as the summer recess for house and Senate is August 7th.

While we are headed in the right direction and while no one knows for certain, this recovery may take a year or longer to return to those previous levels of employment.

Work from the beach

Will this virus be stopped? Yes, we believe (although we are not scientists) that the virus will be quelled eventually (maybe in early 2021) through a vaccine and/or therapies to heal and reduce mortality. Masks may be here to stay for the time being. Today, there is no truer statement than Plato’s famous words: “necessity is the mother of invention.” New ways of working and getting healthcare are evolving such as Zoom meetings and having a doctor visit via telemedicine. Technologies are being created to help us adapt to a world where we can transition easily to and from remote work environments as needed. New safety protocols such as plexiglass shields, floor decals, seat protectors, and office dividers are being produced to help businesses get back to work safely. And, for those who want to be on vacation without leaving the office, the dream of working from the beach is no longer just a dream.

The coming months

Stock performance is likely to be uneven, and all boats may not rise with the tide, i.e. certain sectors may do better than others. Recently, we saw busy shoppers at certain home goods and hardware stores so it’s not surprising to see that year to date, home improvement stocks have advanced 20X more than S&P 500. However, since no one is going anywhere or not heading out to eat, airlines and restaurants are down significantly more than the broad market. Now, more businesses are re-opening. June retail sales were up 7.5% (https://www.census.gov/retail/marts/www/marts_current.pdf). This, however, may be short lived in some geographies as the virus surge has resulted in some bar and restaurant closings, the Texas capital, Austin, is one notable example. To add to the excitement, there is an election in November which is going to be here before we blink. This may add to a shaky period as the market digests the impact of the election.

At this point, we believe that the future will bring new investment opportunities. Innovation in technology and health care are creating new products and services to make our lives better. The merger and acquisition and IPO’s have started to resurface. Like any investment, time is needed, and an investment time horizon of 3-5 years is reasonable.

We would love to hear your comments and questions.

Stay safe and buy a fancy new mask.

Best regards,

Laura Alspaugh

Michael Kaleel

LFS-3176458-072420

The Market, the Economy & the Virus

April 13,2020

In the wake of this terrible coronavirus (Covid-19) and the disruption and devastation it has caused all around us, we at The Kaleel Company hope this communique finds you and your family healthy and comfortable during this global crisis.

Concerning the stock market activity, I was recently reminded by a friend, a multi-decade institutional manager, that in times of a bear market, all the Bear needs is an excuse for the markets to go lower, sometimes creating more panic selling in the marketplace. However, for the Bull to emerge and lead the market higher, the Bull needs a reason. Sometimes it’s hard to find legitimate, convincing reasons to go up. In these last five weeks, we have heard predictions that may have driven the market lower. This has brought fear and uncertainty into our lifestyles as well as survivability concerns for businesses, and ultimately, what the world will look like after Covid-19. It’s been hard to find solid, legitimate, acceptable reasons for the market to go up; however, we see some light at the end of the tunnel.

Oil Prices Collapse, Stocks Prices Collapse, Signs of Improvement

Perhaps you have noticed lower gas prices. Oil prices collapsed 67% in the past 3 months from $61.06 per barrel to $20.09 Monday 3/30/20. As you may recall, this collapse was brought on by a dispute between the world’s # 2 (Saudi Arabia) and # 3 (Russia) oil producers just as the Covid-19 was bringing the worldwide economy to a standstill, resulting in plummeting oil prices as well as oil company stock prices. This brought a shock the market, negatively impacting those invested in growth and income strategies. Recently oil prices have risen, yet still markedly lower than at year end. The oil market may be starting to stabilize and may present opportunities. (source: BTN Research).

Protection for small businesses

The mad dash for cash by small businesses started last Friday (4/03/20). The “Paycheck Protection Program” (PPP) in the recently passed Washington legislation provides loans (through SBA-approved lending institutions) as high as $10 million that will be forgiven when used for payroll costs (including benefits), rent and utilities. (source: CARES Act). The US Government has stepped in to support Main St. and small companies. With roughly half of the economy driven by small companies, this much-needed cash will undoubtedly make a positive impact and help to keep these companies afloat.

Rapid race to find a treatments, faster testing or vaccine

Clearly the best minds across the globe are searching for a cure that will allow people to return to a level of normalcy. Various treatments are being highlighted in the news and trials are beginning to happen: this is positive news. How long it takes to find a solution is dependent on many factors, but it will come. The US and the world have had past health crises, and cures were found. This is a tremendous opportunity for all of us to benefit from new drugs, new technologies and emerging new companies.

More pain may be on the horizon

We all know that unemployment is going to be quite high due to the shutdown of businesses across the US. Most agree that small and large company earnings will be damaged, so it should be no surprise the next two to three quarters could be disappointing. We believe that the monetary policy and fiscal response by our government has not been fully appreciated, and we have not seen the full benefit yet. Yes, there is a lot of bad news out there, but there continues to be a trickle of positive news, which has caused the stock market to have some significant up-ticks over the last few weeks. We are looking and planning to make investments for one, two, and three plus years into the future. One must look beyond the next six months. While it is gloomy, and we really do not know how long Covid-19 will last, we believe that at some point it will be under control. Our focus is on companies that are well financed, industry leaders, and should fare well in this environment.

Our world has changed in 5 weeks in ways we could have never imagined. The first US death from the Covid-19 was reported on 2/29/20. The horrific national death total topped 10,000 this week. This war – against an invisible, microscopic virus – is unlike any war in our lifetime. It’s a war in which all people, Americans and citizens of every country across the globe, are on the same side. Stay home and stay safe (source: BTN Research).

Best regards,

Michael

LFS-3034417-040820

Update on Market Sell-off

03/20/2020

Boy, what a day in the stock market it was! After listening to the news this weekend concerning the lack of agreement between Russia and Saudi Arabia on oil production, I wondered how deep a reaction we might see in the markets. I woke up Monday and what a jolt it was to hear and read the news regarding the foreign markets and the US futures. A sell-off at the opening bell caused the markets to halt trading for fifteen minutes to regain stability. With all this frightening and negative news, it is difficult not to be worried and unhappy.

We believe that there are three factors that are attacking the stability of global stock markets. The first is the coronavirus which we wrote about last week; the numbers continue to rise. The second is the dramatic slide in oil prices due to the Saudi’s and the Russians being unable to agree on production cuts. The third is the longer-term threat of weakening earnings and profits due to a potential slowdown in business.

Clearly the virus in and of itself continues to be a big concern. There is a lot of conflicting news from the medical profession, consultants and advisors. The consensus is that the virus will be contained but when and how is unclear. Stemming the spread of the virus at least for now is proving to be difficult. However, many towns, cities and state governments are working on systems to contain this virus while we wait for a cure. The virus is a top of mind issue that has the potential to slow down commerce for a while. After listening to all the experts, no one knows what the time frame will be. That said, we believe that the virus will either fizzle out on its own or medical research will find a cure.

The second factor is oil prices plummeting due to OPEC talks. The oil industry stocks have taken a big hit; the energy sector traded down over 20%. The disruption in oil prices is because Russia walked away from talks on production cuts, and as a result, Saudi increased production and slashed prices. We believe this situation cannot continue. In our opinion, they will reach an agreement, and that will stabilize this market. We view this as a short-term disruption which will resolve itself.

Based on reaction to the negative news from the above two concerns, the stock market is pricing in lower future earnings and lower multiples resulting in lower price to earnings ratios thus lower stock valuations. The 10 Year US Treasury yield’s unprecedented decline to 0.51% is lower than the current rate of inflation. What this means to investors is that buying US Treasuries is a losing proposition because inflation destroys purchasing power. Ultimately, these low rates are not likely to be satisfactory to investors, pre-retirees wanting to grow assets, and retirees needing income. The dividend yield on many stocks is substantially higher than the yield on a 10-year Treasury, and many big-name growth companies are now selling at much lower prices. We believe that once these opportunities are realized, money should return to the equity markets.

This is a time not to overreact but also not to ignore. We have raised various levels of cash based on client’s needs. At some point, there will be opportunities to put that cash to work. The US and foreign market sell-offs are creating a lot of anxiety for everyone. Keep in mind that the oil issue should be resolved, and the virus will be contained at some point.

Please don’t hesitate to call anytime to talk and discuss your questions or concerns.

Sincerely,

Michael

LFS-2987504-030920

The Coronavirus & the Election of 2020

03/03/2020

Last week, the stock market’s reaction to the spread of the Coronavirus (Covid-19) was severe, declining 11%. investors preferred bonds, driving interest rates even lower with the 10-year US Treasury remarkably below 1.10%.

China swiftly addressed the virus by shuttering down manufacturing facilities which delay sending needed supplies and parts from China to the US. For US companies, the concern is that US earnings will be negatively impacted due to production delays, and stock prices dropped last week to a level consistent with lower earnings. The Federal Reserve has acknowledged that this virus should slow economic growth by affecting the global supply chain. This drag on the economy could continue into the summer, but no one knows for sure.

With the election coming into the forefront and a spreading virus without a cure, we believe that the markets will continue to be volatile. With respect to Covid-19, we have experienced this before with SARS, swine flu, and Ebola. While this is a very difficult and frightening illness, research is being done rapidly to find a vaccine. The negative impact of this situation is likely to diminish with a vaccine, but we certainly don’t know when that time will come.

Some might say that exogenous events like a rapidly spreading virus have the potential to push economies into recessions. We don’t know if this is the case here. What we do know is that Covid-19 has come at a time when our economy is in good health. Our economy should be able to experience this as a short-term hiccup.

Last Friday’s market was struggling to come off the week’s lows, and Monday’s sharp stock market rebound is possibly anticipating an interest rate cut by the Fed as well as support from foreign central banks. With lower short-term rates, companies can borrow cheaply and to do what is needed to get through this difficult time, e.g. finding or creating new supply sources. Also, with lower long-term interest rates, homeowners and potential buyers are in a great spot to refinance a mortgage or to borrow to buy a new home.

The combination of low interest rates and extremely low unemployment is a strong underpinning to our economy and should keep consumer confidence high. With consumer confidence strong, we believe that stock prices will rebound.

Best regards,

Michael

LFS-2976925-030220

The Yield Curve, a Recession, and Thoughts about the Future:

Straight Talk about Yield Curve Inversions

10/01/2019

Perhaps you’ve read or heard enough about yield curves for one lifetime. Nonetheless, we are sending you this piece to give you a little background and education on the much talked about yield curve and what all the fuss is about.

Friends, clients and relatives have been asking us about the significance of an inverted yield curve. We thought we’d take a minute to give you our thoughts on this topic which continues to be of interest to many experts on economic and financial matters.

What is a yield curve?

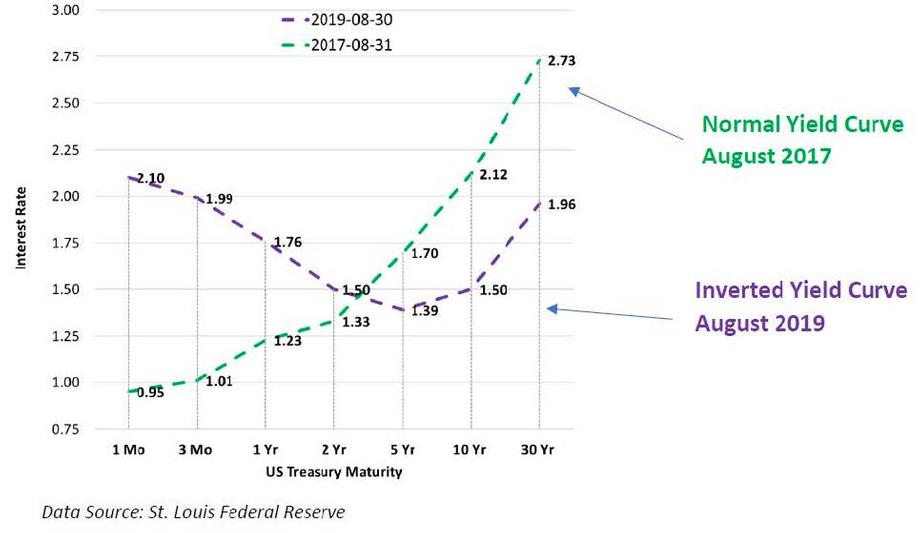

For those who wondering what the yield curve is, it’s the term used to describe the how US Treasury bond interest rates vary for a set of time periods, i.e. for 3 months, 6 months, 1 year, 5 years all the way to 30 years. The reason is it called a “curve” is because when one plots it as a line on a graph, the line is an upward sloping “curve” in “normal” economic times with short term rates lower than long term rates. The yield curve shifts based on various factors in the economy.

The inverted yield curve

Two years ago, we had a yield curve (green line) that was upwardly sloping, a normal shape with low rates for the 1-month US Treasury (0.95%) and much higher rates for 10-Year US Treasury (2.12%).

At the end of August, the rate on the 1-month US Treasury is significantly larger at 2.10% than 1.50% for the 10-year Treasury. That is the inversion. The Federal Reserve Bank began raising the Fed Funds rate creating higher short rates.

Yield curve inversion and recession

Since post World War II, an inverted yield curve has been an accurate predictor of recessions (defined as two consecutive quarters of negative Gross Domestic Product). The funny thing is that by the time we see the evidence in the reported GDP, the recession has already happened.

The problem with trying to predict a recession is that we cannot be sure when it will occur or even how severe a recession it will be. Most US recessions have been short lived. 2008 was severe because it was triggered by a host of factors which we won’t regurgitate here.

Should I remain invested in stocks if a recession is coming?

If an inverted yield curve is signaling a recession, you might ask, “Shouldn’t I just get out of stocks until the recession is over?”

If we could predict the future and get the timing just right, then maybe yes. But the practical answer is no… do not get out of your stocks. Companies still make money in recessions. Some stocks even provide protection in recessionary periods, utilities, consumer goods companies, healthcare for example. Ultimately the recession will recede! Optimism prevails and growth returns.

Where is optimism found?

Talk of recession and an end to the post-2008 expansion is everywhere. Seems like pessimism is far more prevalent than optimism these days. But, if you step back from the noise, you will realize that creative energy is abundant in our country and around the world. Climate change is driving innovations in energy and fuel storage. Businesses are working on increasing sustainability in agriculture and food. Businesses are creating things that to make lives easier and allow us to do more in less time. Self-driving cars and other technologies will help our aging population continue to be mobile and lead longer and healthier lives. The rate of change and innovation will be staggering. Remember when the phone wrist watch was just a cartoon idea? Apple made the phone watch a reality.

Investors will fuel this innovation resulting in investment opportunities. The next recession will come and will go, but equity investing will persist because opportunities to make money will continue. Don’t get caught up in headline news. And if you are concerned about the future, we take a page from Mister Rogers who advised children to “Look for the helpers.” We recommend thinking, “Look for the innovators and the optimists.”

What should I be doing if a recession is coming?

It’s a good time to review your portfolio and understand how you are invested.

Look at your personal expenses and perhaps try to put more cash aside in case you need it. Having cash on hand is a good thing to have all the time but even more important during a recession.

Is your equity portfolio diversified or are you concentrated in one area of the stock, either “growth” area or “value”? Large cap equities or small cap equities?

Rebalancing your portfolio, particularly if equities have risen to become a greater percentage than you might want at this point and stay the course with the appropriate level of stocks for your age and situation.

Market Thoughts and Update

March 1, 2018

To Our Valued Clients & Friends,

The fear of an all-out trade war gripped Wall Street last week, driving stock prices down to near calendar year lows. With just 4 trading days remaining in the first quarter 2018 (the markets are closed this next Friday), the S&P 500 is down 2.8% YTD (total return). A negative quarter would break the index's streak of 9 straight positive quarters and would be just its 2nd down quarter in the last 5 years. The S&P 500 has had 20 trading days YTD that have resulted in at least a 1% gain or loss, more than double the 9 such trading days that the index experienced in all of 2017 (source: BTN Research).

Ironically, by the time the contentious steel and aluminum tariffs became effective last Friday (3/23/18), 32 additional countries had been added to the exception list from the original 2 exempted nations – Canada and Mexico. All 28 European Union (EU) countries plus Argentina, Australia, Brazil and South Korea, received last minute suspensions from the 25% steel and the 10% aluminum tariffs. Further exemptions are expected over the next 5 weeks (source: White House). Clearly the tariff situation is looking much less draconian.

The US government came within 11 hours of its 3rd government shutdown this year, but ultimately Congress and the White House agreed on federal spending levels for the fiscal year which will be half over later this week. Legislation signed by President Trump funds the federal government through 9/30/18 and allowed both parties to claim victory – Republicans increased military spending by $66 billion over its 2017 level and Democrats added $52 billion to domestic programs. Apparently, “Fiscal discipline” is simply not a popular concept held by many current Washington lawmakers (source: BTN Research).

Notable Numbers for the Week:

HALF OF ONE PERCENT - The Federal Reserve began a rate-tightening cycle on 12/16/15. In the 27 months since then (through Friday 3/23/18), the yield on the 10-year Treasury note has increased 0.52 percentage points from 2.30% to 2.82% (source: Treasury Department).

ENERGY INDEPENDENCE? - American oil producers have pumped at least 10 million barrels a day of crude oil for the last 7 weeks, hitting 10.407 million barrels per day for the week ending Friday 3/16/18. The last time US oil producers hit 10 million barrels a day of crude oil was in 1970 (source: EIA).

ONE MONTH - The US government ran a $215 billion budget deficit in February 2018. Until 1986, the government had not recorded an annual deficit as high as $215 billion (source: Treasury Department).

DEMOGRAPHIC SHIFT - By the year 2035, the projected number of Americans seniors aged 65 and up (78.0 million) will exceed the number of American children under the age of 18 (76.4 million), the first time in US history that will have occurred (source: Census Bureau).

I hope you found this email helpful and informative.

Best regards,

Michael

Reproduction Prohibited without Express Permission. Copyright © 2018 Michael A. Higley. All rights reserved. The content of this material was provided to you by Lincoln Financial Securities Corporation for its representatives and their clients.

Securities offered through Lincoln Financial Securities Corporation, (Member SIPC) a broker-dealer. Past performance isn't indicative of future performance. An index is unmanaged, and one cannot invest directly in an index.

This e-mail may include forward-looking statements that are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied.

03/26/18 Monday LFS-269527-032618

FEBRUARY 2018

To our valued clients,

The market's recent volatility has surprised many investors and has created headline news. While the sudden onset of volatility is unsettling, it's certainly not unexpected. To help allay your concerns, we'd like to share our perspective on the reasons for the recent market volatility.

A summary of the market

Global equities turned in a greater than 20% return in 2017. The momentum carried over into 2018 with a continuation of the advance. Then February brought a quick and powerful reversal. In just a few days, the impressive gains of January were largely erased, essentially leaving markets where they began. After the market close on February 5th, media outlets called the decline the “biggest drop” in history. While this may be true of intraday trading on a point drop in the DJIA, it isn't particularly helpful in assessing the decline.

When viewed on a percentage change basis, the story is considerably different. It was far from the biggest drop ever: on August 24, 2015 the market fell intraday 6.6%, and in May of 2010, it dropped a staggering 9%. As time and markets advanced, those days are now largely forgotten. To state it more accurately, the February 5th decline was the largest drop in 30 months, and only the 99th largest drop in the last 120 years.

This is not to say that we are dismissive or unconcerned about the decline. As an advisor and steward of capital, we are concerned about anything that affects our clients, their portfolios, and their goals. This situation continues to develop and the short-term direction of markets remains unclear. A case in point: On February 6th, equity markets oscillated wildly between losses and gains throughout the day, and ultimately ended up 567 points. Rest assured, we will continue to monitor the market with an eye toward prudent management of your capital.

A historical perspective

While the equity markets have enjoyed several years of low volatility, market downturns are not uncommon over time. It is important to note that the market tends to move in a “two steps forward, one step back” fashion.

A History of Declines (1900-February 2018)

Type of Decline Average Frequency* Average Length** Last Occurrence

-5% or more About 3 times a year 47 days February 2018

-10% or more About once a year 115 days August 2015

-15% or more About once every 2 years 215 days October 2011

-20% or more About once every 3½ years 341 days March 2009

Source: Capital Research and Management Company Past performance is no guarantee of future results.

*Assumes 50% recovery rate of lost value

**Measures market high to market low

Until recently, volatility in the markets had been uncharacteristically muted. As unsettling as it is, this may merely be a return to a more normal market environment. Over the past two years, the markets marched steadily forward. Importantly, through January 2018, the S&P 500 advanced 15 straight months on a total return basis. It is a typical human trait to become less accustomed to events when they become less frequent. The recent declines in the markets become more painful to many because they seem less common. These perceptions, however, don't alter the fact that periodic declines are both common and unavoidable.

What happens now?

We focus on what is happening in the economic environment rather than the daily price changes of the indices or individual companies. The current environment continues to be on good economic ground. The news outlets will want to keep you engaged and tuned in to their stations by stating this was the “largest drop” or the “fastest decline” since whenever. These statements can get many people agitated; however, the worst possible reason to make changes is the emotional reason.

We realize that market declines are unnerving to even the most disciplined investor. A great quote on what to do in times of market corrections comes from John Bogle founder of the Vanguard funds. When faced with a serious market sell off he said, “Don't do something, just stand there." This is sound advice on how not to react from a great investment expert.

Please don't hesitate to call with answer any questions or concerns.

Best regards,

Michael Kaleel

LFS-2020997-020718

*This message is intended for the use of the addressee and may contain information that is privileged and confidential. If you have received this message in error, please erase all copies.

*Investments offered through representatives of Lincoln Financial Securities, Member SIPC. Michael M. Kaleel, Branch Manager.

*Advisor services offered through representatives of Kaleel Investment Advisors, LLC. Michael M. Kaleel, Registered Investment Advisor.

*The Kaleel Company, Inc. & Kaleel Investment Advisors, LLC. and Lincoln Financial Securities are not affiliated.

Michael Kaleel, CLU, ChFC

President

Financial success today requires complex problem solving to manage the risks you see, and those you don't.

Recognized in the financial industry as a leader and complex problem solver for uncommonly successful individuals, Michael Kaleel and his team of specialists use their intellectual capital to create sophisticated insurance and investment solutions.

info@kaleelcompany.com | www.kaleelcompany.com/

STAY CONNECTED

![]()